Advertising budgets have swung away from mass media, towards short term direct online communications, at the expense of long-term brand building.

Not that long ago (well back in 2001) I could share a throw-away barb around the latest Nescafe advertisement with you and expect a smile because you could relate to the same shared experience. Today it is highly unlikely that you have shared the same brand advertising experience as I, in a very long time.

Brands are shared stories

Not that long ago I could harp on at my surprise at the latest developments in a popular TV crime thriller series, knowing that my colleagues had watched the same show last night. I could recognise that annoying tune a stranger was humming in the elevator as it was played too often on the radio. I could pass judgement be it laughter, slander or interest at the latest advertisement for Cadbury, Carlsberg or Nescafe.

Shared brand experiences are no more

What was once woven into our shared community experience may no longer be preceded with the word “shared”. The advertisements I see are very different from those which my friends see. When I listen to a concert on YouTube the advertisements that I am served differ from others, my Spotify playlist is radically different than the stranger in the elevator, after all, she has never heard of INXS. My office colleagues might enjoy Sherlock, but it is just not thrilling enough for me. Even the news headlines my best friend sees in his Guardian news app, differ to mine (I did vote for Brexit after all); never mind the variation on advertisements served at him by Google and Facebook.

A brand once communicated shared trust

One of the core tenants of brand building is to generate a shared trust towards a brand. Such that the brand is considered acceptable, popular even, perhaps aspirational, to others just like you. The brand simplifies our choices, a heuristic, for us to say; “that will do, it is a brand I recognise, it is common, it is popular, I trust it or even merely that this brand will do me no harm”.

Shared advertising experiences are rapidly disappearing, as fast as media is being personalised by the ability to amass data on us (to farm us) and serve personalised content and advertising. Be this programme recommendations (Netflix), music recommendations (Spotify), stories and ads (Facebook), ads intermingled with search (Google) and news (news app).

Media once shared, is now enjoyed in isolation

The decline in shared advertising experiences is augmented by the lack of shared screens, we have moved from a shared TV or radio to individual smartphones screens and headphones. TV stations once sold TV-watching households, magazines harped on about subscribers and sold pass on readership and radio stations sold drive time audiences.

You and I are now the product, unwitting data points

Today we are farmed for improved individual targeting. We are sold to brands as individuals, no longer are advertising sales anchored to a shared audience organised around a popular TV crime series, a magazine’s sports content or radio’s’ drive time slots.

Our media content today is largely free, provided we can be sold to advertisers to fund this free information, entertainment and increasingly communications. All that convenience and content delivered to us on our smartphone comes as a price, we are the product and we are sold, resold, repackaged and resold over and over. Explore some of the data shared with Facebook to help them target you more precisely. When I downloaded Facebook’s data on myself, it amounted to 228 megabytes, a dull 228 megabytes, but an excessive amount of information.

Take the time to read those opaque terms and conditions we agree to in order to use that air quality, ride-hailing or payment app. Read how journalist tracked the movements of US politicians. If Cambridge Analytica were to be believed, we are farmed down to the ability to stop us voting or nudge us to vote for the desired candidate.

The money involved has grown exponentially, online will account for 50% of all advertising expenditure in 2020. The concentration of advertising expenditure reached one in four dollars being spent on Facebook or Google in 2018 and is accelerating.

Facebook, Google and numerous data brokerages have in excess of a million data points on each of us, way beyond our political leanings to enable targeted advertisements to nudge our behaviour in desired directions. The only common mediums that still enable a shared social context are cinema, radio and outdoor display. Today if you and I don’t use the same elevator bank, then it is highly unlikely that we have seen the same advertising in a very long time.

Brands now follow our data footprint

Brands buy our data footprint, not the shared audience for a TV crime series. Brands naturally follow us as they seek to nudge our behaviour, they follow us to where we enjoy all forms of media content. They will use product placement in our favourite Netflix shows, target us on Facebook, push us an offer on our health apps, bug use when we are searching online and pay for e-commerce recommendations to us. Less and less are they paying for TV-watching households, drive time audiences and pass-on readership.

Less and less shared brand advertising experiences, in turn, lead to less shared trust and value (equity) in brands. The narrower the audience, the fewer inroads a brand will make into, our shared familiarity, popularity and trust.

In turn, the less resilient is the brand to a disruption (retailers on the British High Street), a product recall (e.g. Samsung Galaxy Note 7), a public relations mistake (e.g. Gillette #metoo advertisement).

Further, less able is a brand to evolve its logo, its pack design nor extend its range with a new variety. The less able is a brand to rejuvenate, to leverage its brand assets, re-launch to remain relevant to the next generation, nor launch new products and services.

Brand building has lost the shared brand story

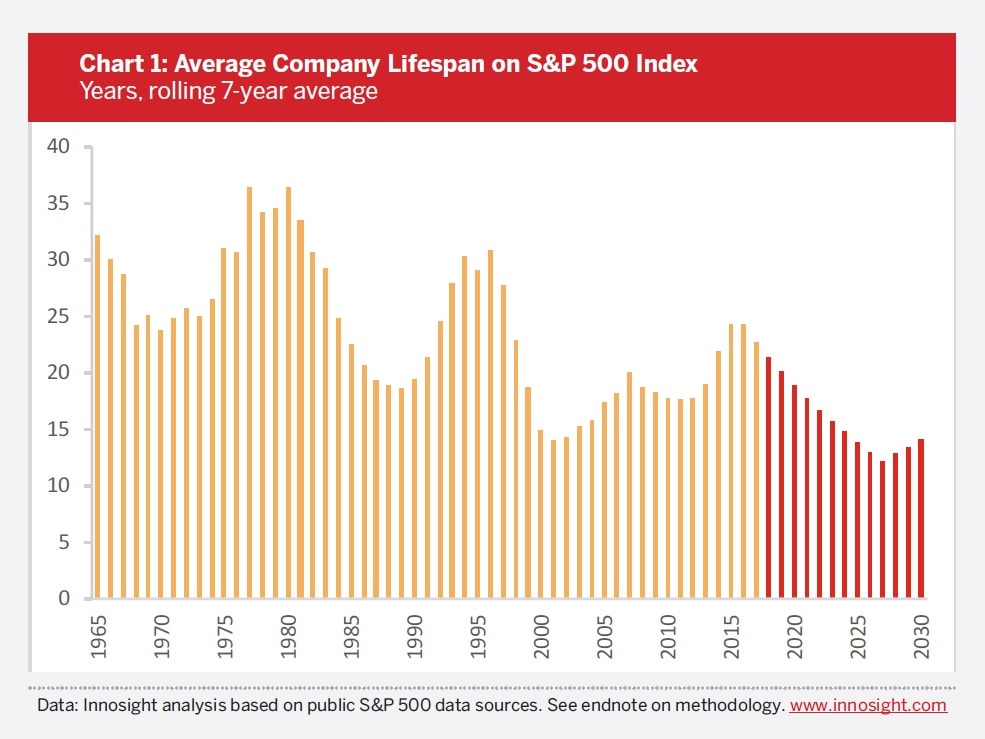

As brands invest less in shared experiences, in shared media and fewer bricks and mortar retail outlets, they have rapidly exited our shared consciousness. Using corporate lifespans as a gauge, the prognosis is a little bleak as their lifespans falter at an ever-increasing rate.

Advertising when individually targeted buys you and I as isolated data points. It is better-targeted mass marketing using data-driven media buying. It harks back to an era of direct and catalogue marketing (circa 1965-1985), in that it is measured in direct conversion responses; click, lead generation, sign up, sale, cross-sell, upsell, recommendations and referrals. It encourages affiliate marketing, clickbait and sensationalised headlines.

Influencers and their false metrics, massive online fraud, smartphone click farms, bot factories, a broken transparency promise, personal data breaches and incongruent and disparate data sources with false metrics mask and confuse the true return on investments in this era of online data-driven direct marketing. Not that understanding the return on investment was any better when buying TV, print nor radio advertising.

Recent studies have proven that only half of the online advertising spend today reaches publishers, with a myriad of middlemen taking their cut within the buying ecosystem.

Marketing professionals’ pursuit of these misleading metrics leads to two extremes of advertising formats. Neither of which build a brand into a shared experience which tells a brand story and helps to grow the brand’s value over time nor protect the brand in times of distress. They can propel short term sales, lead generation or reviews.

The first format of advertising in an online banner or post that is tactical at best, functionally skewed, promotion driven and rarely capable of hitting the basic creative tenants of great advertising (see Advertising that works below).

You and I can create an online display advertisement with a call to action and get an industry average of 0.35% click-through rate on Google and 0.89% for Facebook. But creating an online advertisement, where the combined image and headline, stop us in our tracks, grab attention, make us think and help anchor the brand positively in our memory is a true and rare creative talent.

The second format is the surrogate for TV advertising; video. YouTube announced advertising revenues of US$15.5 billion in 2019 more than US TV networks ABC, NBC and Fox combined. Increasingly Video has become a long play, where the story requires the audience to watch for not a mere 30 seconds, but 2 to 6 minutes. Off course YouTube and Facebook reinforce this approach, reassuring us that all is well because 30 seconds of play count as a view on YouTube and a mere 3 seconds of play count as a view in Facebook (hence why the autoplay function is the default setting). As if that is not enough fraudulent “views” can be bought.

Even if you and I can create a brand story that meets the tenants of great advertising, only the best creative minds can meet the challenge of delivering that story in a 30-second advertisement spot.

Advertising that works

From Cimigo’s empirical research from testing over 400 videos highlights adverting that works, we have learnt these eight tenants:

- Creative hook – which is integral to brand or message.

- Brand integrated into the story – not merely by association.

- Think campaign! – think of a campaign idea. Not a single video.

- Own brand cues and styles – dramatically improve efficiency.

- Keep it simple – really simple! – say less and communicate more.

- Break category advertising expectations – stop advertising the category.

- Resonate by tapping into emotions – social responsibility, pride, family values, culture, humour is a powerful tool as is a feel-good factor.

- Credibly convincing – new news is not always essential but helps convince. Dramatise with purpose or humour.

We have ignored the empirical evidence

Since the first banner advertisement in Wired’s (hotwired) online magazine back in 1994, the promise of a new era of digital marketing with transparent returns on media and advertising investments has never materialised. Advertising and media agencies have followed the money and caved in the face of being labelled “traditional” and “out of touch”.

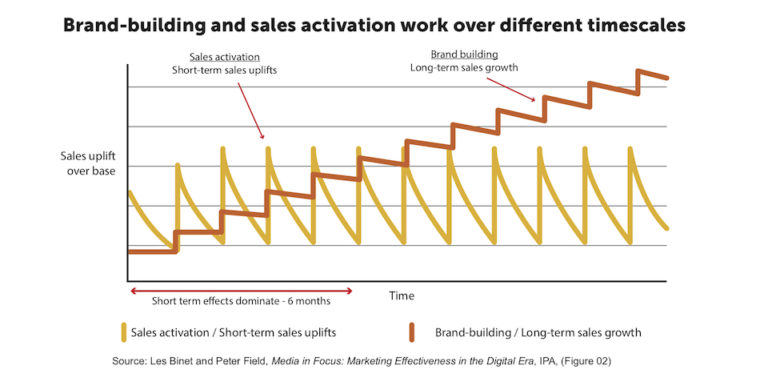

The most empirical work to date conducted by Les Binet and Peter Field, Media in Focus: Marketing Effectiveness in the Digital Era, IPA has proven that the optimal ratio of expenditure between brand-building communications and sales activation is 60:40.

Yet for many brands, the imagined budgetary pendulum has swung far more to activation spend (mostly online) and away from brand-building communications. Below is their summary, if you read only one of the hyperlinks in this article, this is the one to read;

- Budget is one of the most important determinants of campaign effectiveness (second only to the creative work in importance).

- Share of voice is an important metric. The rate at which a brand gains market share tends to be proportional to its “extra” share of voice defined as the difference between the share of voice and market share.

- The balance between brand and activation also matters. A 60:40 ratio of brand to activation spend is typically optimal.

- Sales activation works best when focused on people who are likely to buy now or very soon. Tightly targeted media work best for activation.

- Brand building takes more time, and requires repeated exposures, often over months or years. The target audience may not be buying for some time, and are not necessarily interested in the category right now.

- Brand effects are enhanced by social amplification and herd behaviour. ‘Fame’ strategies that get everyone talking about a brand are extremely powerful and efficient, despite the seeming ‘wastage’ involved.

- The long-term, social nature of brand building favours broad-reach media, rather than tight targeting.

- For sales activation, rational messages tend to work best, so information-rich media are useful (ideally with a direct response mechanism).

- For brand building, emotional priming works better. Audio-visual channels excel here (and music can play a surprisingly big role).

- Online channels make offline media more effective, and vice versa.

Big brands are not built online

Most experienced marketing professionals would not advocate for online communications alone, however, there are far more inexperienced people propagating an online-only solution. Consider for a moment these two questions;

- Think of an example of a great brand that has been built online?

- Think of an example of a great online advertising campaign, that alone was game-changing (i.e. shifted sales or market share significantly) for the brand?

I am normally met with silence from online advertising advocates or given the same example of the Old Spice campaign.

Big brands are rarely built online. Local neighbourhood brands can be built online, a local store or restaurant, books can reach a very targeted audience online and create momentum. I can seek referrals and reviews online to help build trust. The online world has a very long tail of niche interest groups that can create shared spaces for passionate interest groups to meet, share and for brands to reach them.

But again big brands are rarely built online. Those that I can think off include online platforms, e-commerce, online media, mobile applications, software as a service, brands run by celebrity CEOs (e.g. Elon Musk’s Tesla) or celebrity (licensed) beauty brands such as Rihanna’s Fenty Beauty.

Big brands cannot be maintained online alone

Online advertising alone cannot provide shared brand experiences and infiltrate society in a way that creates our shared familiarity, popularity and trust. If big brands can rarely be built online then why would we expect them to be maintained online? To repeat one of Les Binet’s and Peter Field’s conclusions; the long-term, social nature of brand building favours broad-reach media, rather than tight targeting. Interestingly Google, Facebook and Amazon will be advertising at the Superbowl 2020, seeking broad media reach.

So why then have the big brands not gone away?

I have sought empirical evidence that big brands are faltering and heading for demise, but I have yet to find it. I can see anecdotal evidence that those aged under 30 have less trust towards big brands than those aged over 40. I can see anecdotal evidence of brands in some categories losing relevance to consumers. However, the evidence is not definitive beyond expected brand life cycles.

Perhaps the demise of big brands is not imminent, however, I do believe that too many large brands are resting on their heritage and their investments in the brand over previous decades (and for many brands over centuries). At 50 years of age, it works for me, my trust was built long ago and reinforced through my brand behaviour. For my 18-year-old daughter, most big consumer good brands hold very little relevance. At some point, perhaps a demographic tipping point, will this malaise lead to an outright demise?

Before this becomes a history lesson, I do urge all of us all to regularly recalibrate our marketing channels and play a brand-building game that goes beyond our own job tenure and that will leave our successors with a strong brand. We must invest more in long term brand building than we do in supporting sales with short term activations. We must use all channels which are fit for purpose, both online and offline, with an understanding of the metrics and their limitations. If we do not, I fear our successors will accuse of as having followed the pied piper down the abyss of advertising’s worst hyperbole.