Celebrating 19 years of market research today. A huge thanks to all the team at Cimigo (past and present) for making the last 19 years such a wonderful journey. Thank you to all our clients for trusting us to help you make better choices.

Celebrating 19 years of market research today. A huge thanks to all the team at Cimigo (past and present) for making the last 19 years such a wonderful journey. Thank you to all our clients for trusting us to help you make better choices.

Changes in Vietnamese consumer behaviour during Covid have intensified during the series of city-wide social distancing measures that have impacted cities across Vietnam in late May and June 2021. This article explores the key changes impacting consumer dynamics in Vietnam.

Richard Burrage

8 minute read

Household financial pressure puts the brakes on Vietnamese consumer discretionary expenditure. One of the most prominent changes in Vietnamese consumer behaviour is apparent in consumers seeking value for money propositions to reduce the stress on their household budgets.

Vietnamese consumers are holding back long-planned purchases and delaying them until their confidence in their income stability returns. Some changes in Vietnamese consumer behaviour are forced on consumers through social distancing measures. Consumers are not able to spend on out-of-home entertainment, eating out-of-home nor enjoy spa and beauty services.

The winners from changes in Vietnamese consumer behaviour continue to be online shopping platforms, which have further propelled delivery and ride-sharing services. The desire to be contactless and the convenience of mobile payments in Vietnam is diminishing the use of cash on delivery, slightly, a push that e-payments really need.

Temporary positive changes in Vietnamese consumer behaviour exist for numerous fast-moving consumer products relating to hygiene and preventing transmission. As and when Covid dissipates these categories will reverse to their typical growth trajectories last seen in 2019.

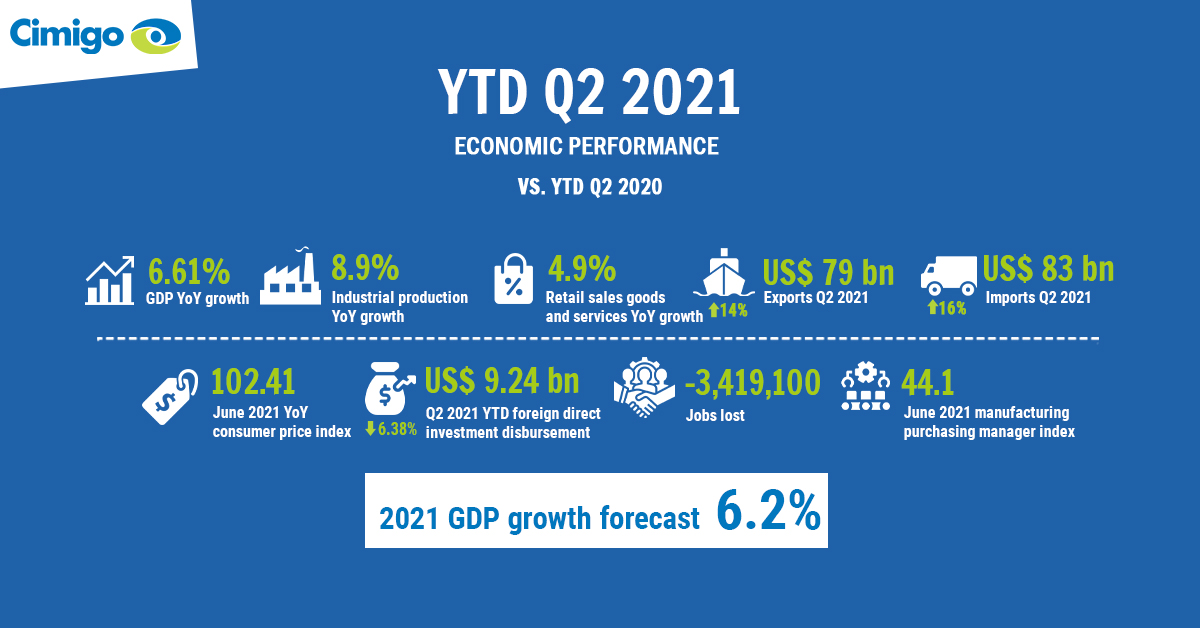

Some households have been hard hit with job losses and lower household income for most households. Whilst the economy continues to grow in the first half of 2021, household incomes are taking a harder hit than they experienced in 2020.

Some households have been hard hit with job losses and lower household income for most households. Whilst the economy continues to grow in the first half of 2021, household incomes are taking a harder hit than they experienced in 2020.

Whilst many, but not all, parts of the manufacturing economy continue to function; trade, services, hospitality and tourism have been curtailed. In 2020 Cimgio reported that the pandemic had reduced annual household incomes by an average of 12%. Job losses have already doubled those experienced in 2020. As of July 1st 2021 Cimigo anticipate the impact will be harsher than 2020 on household incomes, impacting both savings and expenditure. All discretionary expenditure is being re-evaluated.

Whilst many, but not all, parts of the manufacturing economy continue to function; trade, services, hospitality and tourism have been curtailed. In 2020 Cimgio reported that the pandemic had reduced annual household incomes by an average of 12%. Job losses have already doubled those experienced in 2020. As of July 1st 2021 Cimigo anticipate the impact will be harsher than 2020 on household incomes, impacting both savings and expenditure. All discretionary expenditure is being re-evaluated.

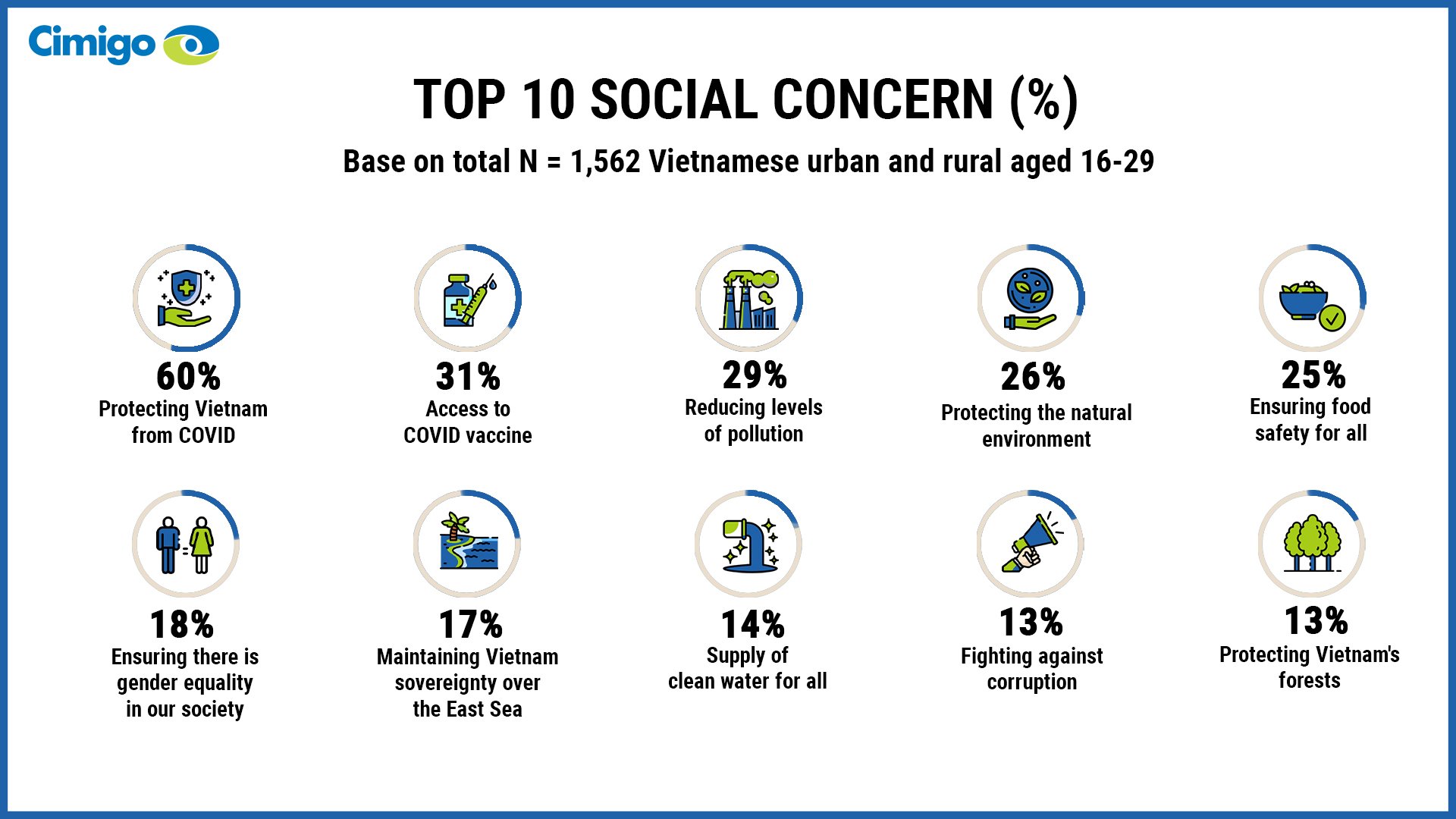

Cimigo’s survey of the digital generation aged 16 to 29, across rural and urban Vietnam in May 2021 found that protecting Vietnam from Covid was the number one concern by a large margin.

4. Vietnamese consumers seeking better value

4. Vietnamese consumers seeking better value Vietnam household income shortfalls derailed the historic premiumisation trends of consumer-packaged goods. One of the most prominent changes in Vietnamese consumer behaviour is apparent in consumers seeking value for money propositions to reduce the stress on their household budgets. Down trading in consumer-packaged goods will continue strongly through 2021. Consumer packaged goods (CPG) are experiencing significant down trading, as consumers are thrifty with their expenditure.

Vietnam household income shortfalls derailed the historic premiumisation trends of consumer-packaged goods. One of the most prominent changes in Vietnamese consumer behaviour is apparent in consumers seeking value for money propositions to reduce the stress on their household budgets. Down trading in consumer-packaged goods will continue strongly through 2021. Consumer packaged goods (CPG) are experiencing significant down trading, as consumers are thrifty with their expenditure.

In 2020 the changes in Vietnamese consumer outlook led to the delay of purchasing new or replacement high ticket price purchases. This has re-emerged as consumers hold back long-planned purchases and delay them until confidence in their income stability returns. Apartments, motor vehicles (2 and 4 wheels), home appliances, electronic devices and home furnishing purchases are all further delayed.

In 2020 the changes in Vietnamese consumer outlook led to the delay of purchasing new or replacement high ticket price purchases. This has re-emerged as consumers hold back long-planned purchases and delay them until confidence in their income stability returns. Apartments, motor vehicles (2 and 4 wheels), home appliances, electronic devices and home furnishing purchases are all further delayed.

Some changes in Vietnamese consumer behaviour are forced on consumers through social distancing measures. Domestic tourism (the one remaining lifeline for the travel and tourism industry since borders were closed to inbound tourists) can no longer travel easily domestically. Most consumer-facing service businesses have already lost six weeks of trading, as they have been subject to more stringent regulations. Consumers are not able to spend on out-of-home entertainment, eating out-of-home nor enjoy spa and beauty services.

Some changes in Vietnamese consumer behaviour are forced on consumers through social distancing measures. Domestic tourism (the one remaining lifeline for the travel and tourism industry since borders were closed to inbound tourists) can no longer travel easily domestically. Most consumer-facing service businesses have already lost six weeks of trading, as they have been subject to more stringent regulations. Consumers are not able to spend on out-of-home entertainment, eating out-of-home nor enjoy spa and beauty services.

The winners from changes in Vietnamese consumer dynamics continue to be online shopping platforms that have already expanded penetration, transaction volumes and “basket’ size over 2020, propelling a massive 54% increase in e-commerce sales in Vietnam in 2020. This ensues with Covid proving a helping push, it has helped the channel build both consumer familiarity, trust and right now dependency.

The winners from changes in Vietnamese consumer dynamics continue to be online shopping platforms that have already expanded penetration, transaction volumes and “basket’ size over 2020, propelling a massive 54% increase in e-commerce sales in Vietnam in 2020. This ensues with Covid proving a helping push, it has helped the channel build both consumer familiarity, trust and right now dependency.

Most service and trading businesses have been working from home. This along with the stratospheric rise in e-commerce has further propelled delivery and ride-sharing services on both the demand side and also the expansion of existing players and the entry of new players.

Most service and trading businesses have been working from home. This along with the stratospheric rise in e-commerce has further propelled delivery and ride-sharing services on both the demand side and also the expansion of existing players and the entry of new players.

Both online gaming and content streaming through the likes of YouTube, TikTok and Qiy have accelerated as consumers have spent less time out of home and more time on their smartphones.

The desire to be contactless and the convenience of mobile payments in Vietnam is diminishing the use of cash on delivery slightly, a push that e-payments really need. The vast majority of shoppers prefer cash on delivery for the control this affords the consumer should products not meet expectations.

The desire to be contactless and the convenience of mobile payments in Vietnam is diminishing the use of cash on delivery slightly, a push that e-payments really need. The vast majority of shoppers prefer cash on delivery for the control this affords the consumer should products not meet expectations.

Numerous fast-moving consumer products relating to hygiene and preventing transmission have experienced strong growth during the pandemic. These include hand sanitiser, masks, even regular bar and liquid soap, body wash and following rumours of Covid festering in our throats, mouthwash.

Numerous fast-moving consumer products relating to hygiene and preventing transmission have experienced strong growth during the pandemic. These include hand sanitiser, masks, even regular bar and liquid soap, body wash and following rumours of Covid festering in our throats, mouthwash.

The following categories have seen a tremendous upside as a result of Covid.

As and when Covid dissipates these categories will reverse to their typical growth trajectories last seen in 2019.

Read Cimigo’s approach on marketing planning to stay ahead of the big bounce back. The pandemic has forced changes in consumer behaviour. Life will not return to normal, a new normal will evolve with new habits and rituals. Consumer mindsets and behaviours have changed, some will be temporary but others will become permanent. These changes will need to be rapidly understood and your product, price, positioning and channel will need to be adjusted.

Contact us at ask@cimigo.com if you need help.

Korean soft power has been nothing but soft, over the past two decades a deluge of Korean TV drama series, music and models has had a far greater influence on Vietnamese pop culture than any other country. This soft power has been instrumental in driving the success of Korean beauty, cosmetic and personal care brands.

Emart is the largest retailer in Korea was founded in 1993 by Shinsegae as the first discount retailer in South Korea. Emart opened the first 12,000 square metre retail store in December 2015 in Saigon, Vietnam with a proposition of a happy hypermarket . Emart has plans for many more stores across Vietnam. Emart is the second major Korean player in the retail landscape in Vietnam after Lotte Mart. Emart should be able to leverage Korean soft power in Vietnam into sales and impact consuemr shopping behaviour. The first store is located at 366 Phan Văn Trị, phường 5, Go Vap, HCMC.

More hot consumer market research trends Vietnam Asia